g_lsq(G;S;Y;XX)

Returns a model corresponding to the multiple least squares regression of one or more independent variables against a given dependent variable.

Function type

Vector only

Syntax

g_lsq(G;S;Y;XX)Input

| Argument | Type | Description |

|---|---|---|

G |

any | A space- or comma-separated list of column names Rows are in the same group

if their values for all of the columns listed in If If any of the columns listed in |

S |

integer | The name of a column in which every row evaluates to a 1 or 0, which determines

whether or not that row is selected to be included in the calculation If

If any of the values in

|

Y |

integer or decimal | A column name denoting the dependent variable |

XX |

integer or decimal | A space- or comma-separated list of column names denoting

the independent variable(s)

|

Return Value

For every row in each group defined by G (and for those rows where

S=1, if specified), g_lsq

computes a multiple least squares regression for the independent variable(s)

XX against the dependent variable Y and returns a

special type representing a model for each group in the data.

g_lsq returns can be used as an argument to the following

functions:param(M;P;I)to extract the regression model parametersscore(XX;M;Z)to score data points according to the regression model

g_lsq may be much slower if there is significant multicollinearity in

the data (i.e., if two or more of the independent variables XX are nearly

perfectly correlated with each other).M is the column containing the result of g_lsq,

use the following function calls to obtain the desired information:param(M;'b';N)Nth coefficient of the model (corresponding to theNth data column inXX)param(M;'p';N)- p-value associated with the

Nth coefficient of the model param(M;'g';N)Nth diagonal value of (XTX)-1, whereXis the matrix of input valuesparam(M;'valcnt';)- Count of valid observations (those where

XXandYare all non-N/A) in the data param(M;'ybar';)- Mean of the valid dependent variable observations

Yin the data param(M;'chi2';)- Residual sum of squares

param(M;'df';)- Degrees of freedom of the model

param(M;'r2';)- Coefficient of determination (R2) for the model

param(M;'adjr2';)- Adjusted R2 for the model

score(XX;M;)- Predicted

Yfor data pointsXXaccording to the model

The standard error of the estimate for the Nth regression coefficient can

be calculated as the square root of the mean squared error multiplied by

param(M;'g';N), where the mean squared error is equal to the residual sum

of squares, param(M;'chi2';), divided by the number of degrees of freedom,

param(M;'df';).

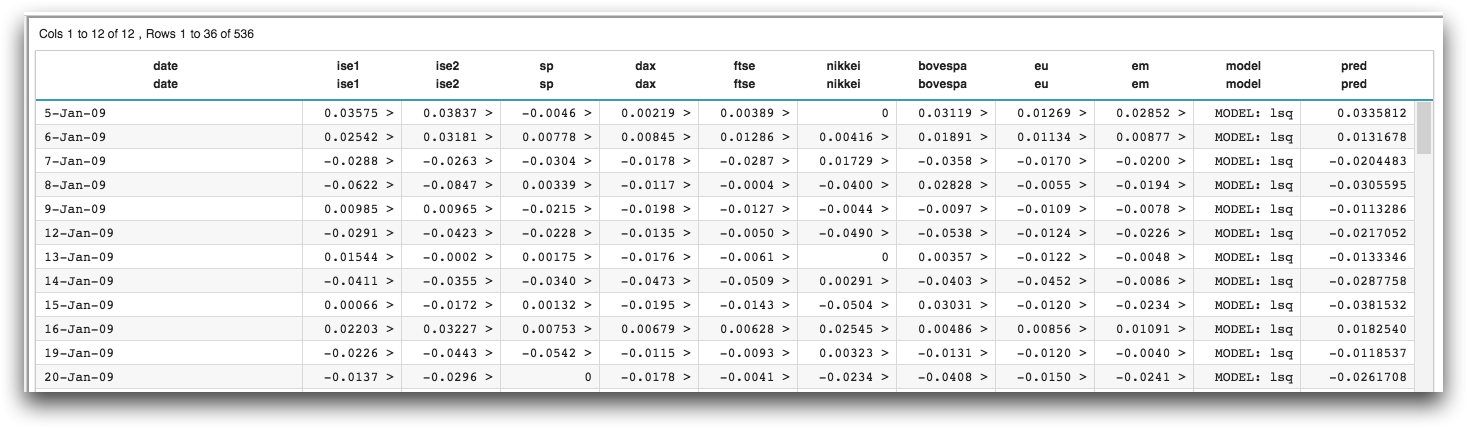

Example

The following example uses g_lsq(G;S;Y;XX) to perform a least squares

regression on a data set containing the returns of a number of international stock exchanges

(pub.demo.mleg.uci.istanbul). It then uses the

score(XX;M;Z) function to obtain the predicted value of the linear

model.

<base table="pub.demo.mleg.uci.istanbul"/> <willbe name="model" value="g_lsq(;;ise2;1 sp dax ftse nikkei bovespa eu em)"/> <willbe name="pred" value="score(1 sp dax ftse nikkei bovespa eu em;model;)" format="dec:7"/>